Navigating the Medicare system can seem overwhelming, especially with its numerous plans, enrollment periods, and options. However, having a clear understanding of its structure and using the right strategies can help you unlock its full potential. Whether you’re a first-time enrollee or someone re-evaluating their current coverage, knowing how to navigate Medicare ensures you get the best value for your healthcare needs.

Medicare plays a vital role in providing accessible and affordable healthcare for millions of Americans. However, understanding its complexities is essential to avoiding overpayments, unnecessary coverage, or missed benefits. This guide will help demystify Medicare, empowering you to take charge of your healthcare decisions with confidence.

Understanding Medicare Basics

Medicare is a federal health insurance program designed to provide essential healthcare coverage primarily for individuals aged 65 and older. It also extends coverage to certain younger individuals with disabilities or medical conditions such as end-stage renal disease (ESRD) or amyotrophic lateral sclerosis (ALS). Its comprehensive structure offers various coverage levels to cater to different healthcare needs.

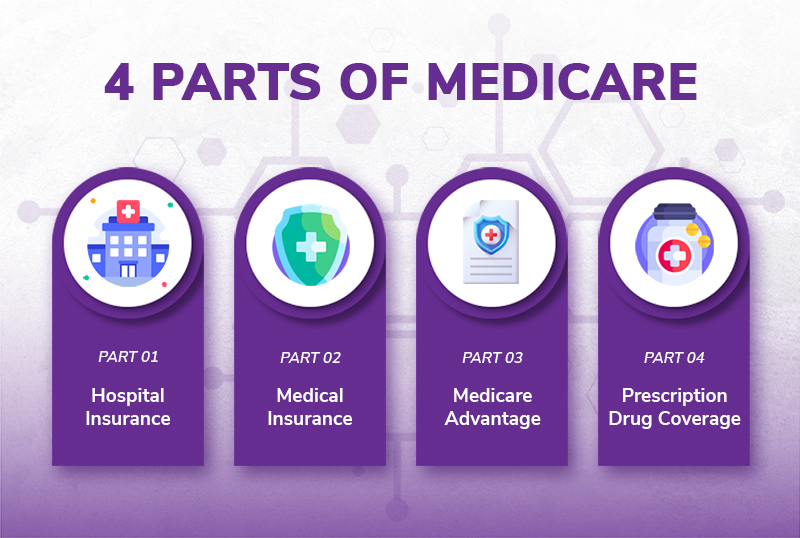

The Four Parts of Medicare

1. Part A (Hospital Insurance)

Part A primarily covers inpatient services, including hospital stays, care in a skilled nursing facility, hospice care, and some home health services. For most beneficiaries, Part A comes without a monthly premium if they have paid Medicare taxes for at least 10 years.

- Who Benefits: Ideal for individuals requiring hospital care or planning for long-term treatment options such as skilled nursing facilities.

- Coverage Highlights: Hospital room and board, medications during inpatient stays, and limited home healthcare services.

2. Part B (Medical Insurance)

Part B covers outpatient care, including doctor visits, diagnostic tests, preventive screenings, and durable medical equipment like wheelchairs or walkers. Beneficiaries pay a monthly premium, which is determined based on their income.

- Who Benefits: Essential for individuals seeking routine care, specialist consultations, and preventive screenings.

- Coverage Highlights: Annual wellness visits, vaccinations, mental health services, and outpatient surgeries.

3. Part C (Medicare Advantage Plans)

Medicare Advantage, or Part C, combines Parts A and B into a single plan offered by private insurance companies. These plans often include additional benefits like vision, dental, hearing, and prescription drug coverage.

- Who Benefits: Individuals seeking comprehensive coverage with added perks like gym memberships or telehealth services.

- Coverage Highlights: Customizable plans, network-based care, and integrated prescription drug benefits.

4. Part D (Prescription Drug Coverage)

Part D helps cover the cost of prescription medications, often making it an essential addition for those with chronic conditions requiring regular prescriptions. Plans are offered by private insurers, with varying formularies and copayment structures.

- Who Benefits: Individuals with regular prescription medication needs.

- Coverage Highlights: Tier-based drug coverage, with varying copayments for generics versus brand-name drugs.

Why Understanding Medicare Is Crucial

Medicare is not a one-size-fits-all program. Your healthcare needs, budget, and lifestyle play significant roles in determining which parts or plans work best for you. Missteps in understanding your coverage options can lead to unnecessary costs, such as:

- Paying for services or medications that could be covered under a better plan.

- Missing enrollment deadlines, which can result in penalties or coverage gaps.

- Choosing a plan with limited provider networks, restricting your access to preferred doctors or specialists.

Taking the time to understand the four parts of Medicare is the first and most critical step toward maximizing your benefits. Whether it’s determining eligibility for premium-free Part A or selecting a Part D plan that aligns with your medication needs, knowledge is key to making informed decisions.

By breaking down Medicare into manageable pieces, you can approach your healthcare with confidence, ensuring you’re equipped to make decisions that save money and enhance your overall well-being.

Review Your Current Medicare Plan Annually

Medicare isn’t static—your healthcare needs and the details of your Medicare plans can change significantly over time. That’s why it’s essential to reassess your coverage every year during the Medicare Open Enrollment Period (October 15 – December 7). Regular reviews help you avoid outdated coverage and ensure you’re getting the best possible benefits at the most affordable cost.

- Check Coverage Changes: Providers often update their plans annually, altering premiums, copayments, and covered services. A plan that worked well for you last year might not be the most cost-effective or comprehensive this year.

- Compare Plans: Take advantage of tools like Medicare.gov’s Plan Finder to compare options in your area. Exploring alternatives can uncover plans with additional benefits, better coverage, or lower costs.

- Look for Cost-Saving Options: Many Medicare Advantage and Part D plans introduce new features, like lower premiums, expanded provider networks, or enhanced prescription drug coverage. Switching plans can lead to significant savings.

Tip: Even if you’re satisfied with your current plan, compare it to others annually—you might discover new opportunities for better savings or expanded benefits.

Understand and Utilize Preventive Services

Preventive care is one of Medicare’s most valuable offerings, helping you maintain your health and catch potential issues early. Best of all, many preventive services are covered at no additional cost under Medicare.

- Annual Wellness Visits: Medicare covers a yearly wellness visit to create or update a personalized prevention plan based on your current health and risk factors. These visits help identify issues before they become serious problems.

- Screenings and Vaccinations: Medicare covers screenings for various conditions, including diabetes, cancer, and heart disease. Vaccinations, such as flu, pneumonia, and shingles shots, are also included, ensuring you stay protected year-round.

- Lifestyle Counseling: Medicare offers support for lifestyle changes, including smoking cessation programs and nutritional counselling. These services are designed to improve your overall health and reduce the risk of chronic conditions.

By taking advantage of these preventive services, you can reduce the likelihood of expensive treatments and hospital visits down the road.

Manage Prescription Drug Costs with Medicare Part D

Prescription drug expenses can add up quickly, but Medicare Part D offers several ways to manage and minimize these costs. Making informed decisions about your Part D coverage ensures you get the medications you need without breaking the bank.

- Choose a Cost-Effective Plan: Different Part D plans have varying formularies, copayments, and premiums. Review your medications against each plan’s formulary to find the one that covers your prescriptions at the lowest overall cost.

- Use Generic Medications: When available, opt for generic versions of your medications. They are significantly cheaper than brand-name drugs but equally effective.

- Apply for Extra Help: Medicare’s “Extra Help” program offers financial assistance for premiums, deductibles, and copayments. If you meet the income and resource limits, this program can save you thousands annually.

- Stay Within Preferred Networks: Many plans partner with specific pharmacies to offer lower costs. Filling prescriptions at a preferred pharmacy can reduce out-of-pocket expenses.

Tip: Utilize Medicare’s Plan Finder tool to compare costs and identify plans that optimize your prescription coverage.

Maximize Savings Through Medicare Advantage Plans

Medicare Advantage plans (Part C) bundle hospital, medical, and often prescription drug coverage into a single plan, making them a convenient and cost-effective alternative to Original Medicare. These plans often come with additional benefits not available in Original Medicare.

- Explore Extra Benefits: Many Medicare Advantage plans include coverage for dental, vision, hearing, and wellness programs like gym memberships or nutrition counseling. These extras can save you money while improving your overall health.

- Avoid Overlapping Coverage: Since Medicare Advantage plans typically include comprehensive benefits, you may not need supplemental insurance. This can prevent redundant coverage and unnecessary expenses.

- Compare Costs and Coverage: While premiums for Medicare Advantage plans are often lower, consider factors like copayments, deductibles, and out-of-pocket maximums. Ensure the plan you choose aligns with your healthcare and financial needs.

Tip: Before enrolling, check whether your preferred doctors and specialists are within the plan’s network to avoid unexpected costs.

Avoid Penalties and Missed Opportunities

Missing deadlines or failing to understand enrollment rules can lead to costly penalties and gaps in coverage. Being proactive about your Medicare enrollment can save you from unnecessary expenses.

- Sign Up During Initial Enrollment: If you’re not automatically enrolled in Medicare, ensure you sign up during your Initial Enrollment Period (three months before and after your 65th birthday). Missing this window may result in late penalties.

- Avoid Late Penalties: Enroll in Part D (prescription drug coverage) as soon as you become eligible to avoid a lifelong penalty that increases your premium for each month of delay.

- Understand Special Enrollment Periods (SEPs): If you experience certain life events, such as losing employer-sponsored coverage or moving to a new area, you may qualify for a SEP to change plans without penalties.

Tip: Keeping a calendar of Medicare deadlines ensures you don’t miss critical enrollment periods.

Use Supplemental Insurance for Additional Coverage

Medicare Supplement Insurance (Medigap) can help cover expenses that Original Medicare doesn’t, such as copayments, deductibles, and coinsurance. For individuals who want peace of mind about out-of-pocket costs, Medigap is a valuable option.

- Explore Medigap Plans: These plans are standardized across most states, but premiums vary. Comparing available plans helps you find the right balance of coverage and cost.

- Coordinate with Medicare: Medigap works alongside Original Medicare, ensuring smoother claims and reducing unexpected expenses. It’s particularly useful for frequent doctor visits or long-term treatments.

- Plan for Long-Term Care: While Medicare doesn’t cover most long-term care needs, pairing Medigap with long-term care insurance can fill this gap, providing comprehensive financial protection.

Tip: Medigap is incompatible with Medicare Advantage plans, so choose the option that best suits your specific needs and lifestyle.

Read More: Medicare in 2025: What You Need to Know About Changes and Benefits

How Guiders Insurance Agency Can Help Maximize Your Medicare Benefits

Navigating Medicare’s complexities can be a challenge, but Guiders Insurance Agency simplifies the process by providing personalized tools and expert guidance. Their platform ensures you can make informed decisions tailored to your healthcare and financial needs.

- User-Friendly Website: Guiders Insurance Agency provides an easy-to-navigate website that enables you to compare different Medicare plans based on coverage, cost, and provider networks.

- Expert Guidance: With a team of knowledgeable advisors, Guiders Insurance Agency helps you understand your options, from choosing the right plan to navigating enrollment periods.

- Comprehensive Resources: From explaining Medicare parts to highlighting cost-saving opportunities, Guiders Insurance Agency equips you with the knowledge to make confident decisions.

- Ongoing Support: Guiders Insurance Agency doesn’t stop at enrollment. They provide continuous support, helping you adapt to changes in your healthcare needs or Medicare policies.

Take Action Today: Whether you’re enrolling for the first time or reassessing your current plan, Guiders Insurance Agency is your trusted partner in maximizing your Medicare benefits. Visit their platform to start your journey toward better coverage and savings.

Conclusion

Maximizing your Medicare benefits requires a proactive approach to reviewing your plans, understanding your options, and leveraging cost-saving opportunities. From preventive care and prescription drug coverage to exploring Medicare Advantage and supplemental plans, taking the time to optimize your Medicare coverage ensures you receive the care you need without unnecessary expenses.

With Guiders Insurance Agency by your side, you can simplify the process and make informed decisions tailored to your healthcare needs. Explore your options today and experience the peace of mind that comes with knowing you’re getting the most out of your Medicare benefits.